Are you wondering how to protect some of your assets from inflation? With inflation hitting the 40-year high BEFORE the war in Ukraine, you might be wondering if only there was something that you could invest in that tracked inflation to keep you from losing your savings to inflation.

That’s where Series I Savings Bonds come in. These are bonds designed to protect the bond holders from inflation. The United States Treasury announces the rates for I bonds on the first of every May and November, and this rate is directly correlated to Consumer Price Index and how it has changed in the past six months. This will allow you to keep your savings even with inflation even if it continues to rise.

The current rate is 9.62% and you will keep earning that for six months after your purchase of I Bonds. You can get this rate through October till the new rate is announced. You will earn the full 9.62% for six months following the date of purchase afterward, the interest will be adjusted to the rate announced in November for six months, and so on.

You must be a citizen or at least a tax-resident of the United States to purchase these as you will need a social security number. You can invest up to $10,000 a year into government I-Bonds online. Additionally, you can purchase an additional $5000 worth of “paper bonds” with your tax return. You can purchase as small as $25 or any penny increment between $25 and $10,000 which makes this a great option for individuals or families with smaller amounts in savings that they still wish to protect.

You must hold the bond for a minimum of 1 year, however they can earn interest for up to 30 years or whenever you want to cash out. It is important to note that if you sell them before 5 years since purchase, you will have to forfeit the last 3 months of interest. After 5 years though, there is no penalty.

This gives you a little more flexibility than traditional bonds after the 1 year waiting period as well. Rather than have to wait for some specific date in the future (potentially many years) for your bond to mature, at any point after 1 year you can take your money back out and only lose a small amount. Consider that if you hold them for one year and immediately sell that is still around 7.2% interest. Still far better than you will find in any other US bank or bond.

If you can, it would be best to hold them for the full 5 years to avoid the penalty. However, if inflation does return back to normal levels and you hold them for three more months at that lower rate of inflation you can also do quite well on your return and protect yourself from the current high inflation rates.

If you have more than $15,000 in savings that you wish to protect from inflation, you may want to look into Treasury Inflation-Protected Securities (TIPS). You can also purchase these directly from the treasury. You can also purchase these through your bank or broker.

The disadvantage to these is that you will be required to pay tax on the interest/increase in principal every year while you hold the TIPS. With I Bonds you can defer tax till you redeem the bond itself. Both are exempt from state & local taxes, but still subject to federal income tax.

Another advantage of I Bonds is that they can be exempt from federal tax (read: tax-free) if used for qualified higher education expenses. You can read more about this here. Currently, at time of writing, to qualify you must have a gross income of less than $98,200 if single, or $154,800 if married filing jointly and this amount changes yearly, check the link above for the current amounts.

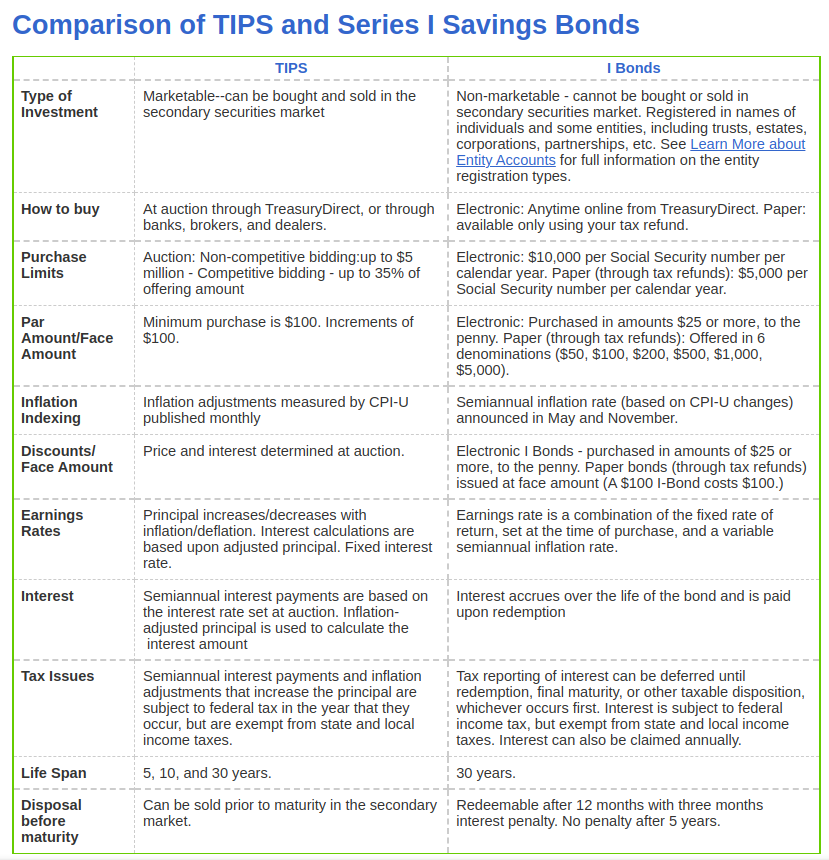

The treasury has a good chart to compare TIPS and I Bonds:

You can create an account on the treasury’s website and purchase I Bonds or TIPS here.